Which Canadian sectors saw the biggest drops?

Payroll employment in Canada declined in February even as average weekly earnings increased and job vacancies held steady, according to new data from Statistics Canada.

The number of employees receiving pay and benefits from their employer—measured as payroll employment—decreased by 60,200 (-0.3%) in February, following an increase of 44,300 (+0.2%) in January. On a year‑over‑year basis, payroll employment was “virtually unchanged” in February, Statistics Canada said in its release.

Average weekly hours worked were 33.3 in February, little changed from January but down 0.9% compared with February 2025.

Canadian employers headed into the second quarter of 2026 with solid hiring plans but mounting doubts about the effectiveness of today’s AI tools, according to a previous report.

Which sectors saw declines?

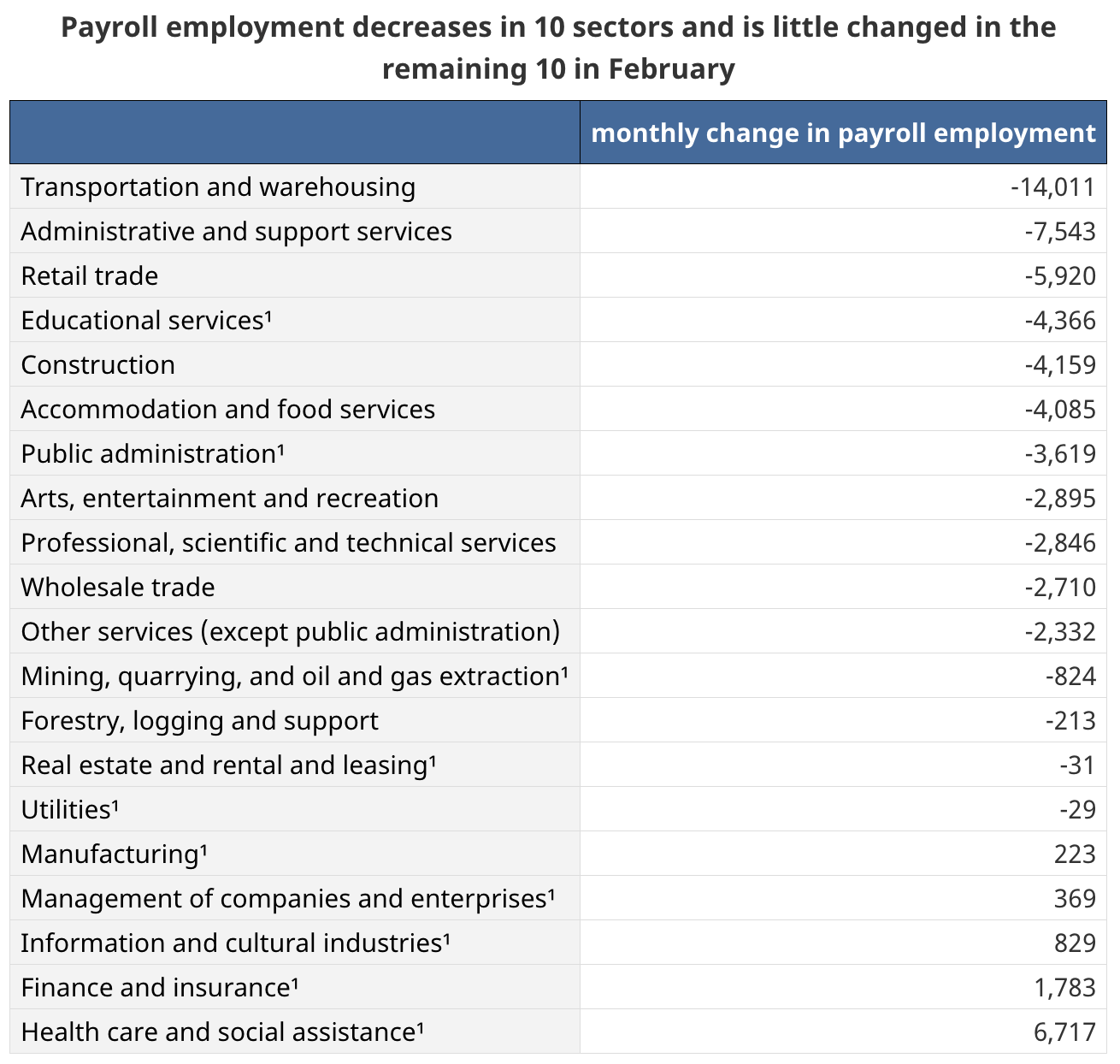

Monthly payroll employment declines in February were concentrated in a handful of major sectors. Statistics Canada reported that the drop was led by transportation and warehousing (-14,000; -1.6%), administrative and support services (-7,500; -0.9%) and retail trade (-5,900; -0.3%).

In transportation and warehousing, payroll employment fell by 14,000 (-1.6%) in February, following little change in January. On a year‑over‑year basis, payroll employment in the sector edged down (-8,000; -0.9%)…led by truck transportation (-4,600; -2.2%) and air transportation (-2,600; -3.0%). These declines were partly offset by gains in warehousing and storage (+1,700; +1.9%) and pipeline transportation (+1,000; +10.5%).

Payroll employment in administrative and support, waste management and remediation services decreased by 7,500 (-0.9%) in February, after an increase of 5,500 (+0.7%) in January. The February decline was “led by services to buildings and dwellings (-2,800; -1.2%) and employment services (-2,600; -1.4%).” On a year‑over‑year basis, payroll employment in the sector was down 8,300 (-1.0%), with business support services (-6,400; -9.4%) and employment services (-4,700; -2.4%) posting the largest losses.

Retail trade recorded its second consecutive monthly payroll decline. Employment fell by 5,900 (-0.3%) in February, following a drop of 7,000 (-0.4%) in January and an increase of 4,700 (+0.2%) in December 2025. Year over year, payroll employment in retail trade was down 26,400 (-1.3%) in February 2026.

The year‑over‑year decline in retail was broad‑based, with the largest losses in clothing and clothing accessories retailers (-9,500; -5.6%), grocery and convenience retailers (-5,900; -1.4%), department stores (-5,800; -5.9%) and building material and supplies dealers (-3,200; -2.3%). Over the same period, employment increased in warehouse clubs, supercentres and other general merchandise retailers, which added 5,100 jobs (+3.2%).

Recently, the Canadian Labour Congress (CLC) welcomed Ottawa’s 2026 Spring Economic Update as a step towards easing workers’ economic anxiety, while warning that the impact will depend on whether new spending and incentives translate into secure, quality jobs.

Earnings and vacancies

Average weekly earnings rose 1.4% month over month to $1,338 in February, after little change in January, according to StatCan. Year over year, average weekly earnings were up 3.4% in February, compared with a 1.9% increase in January. Statistics Canada noted that “in general, growth in average weekly earnings can reflect a range of factors, including changes in wages, composition of employment, hours worked and base‑year effects.”

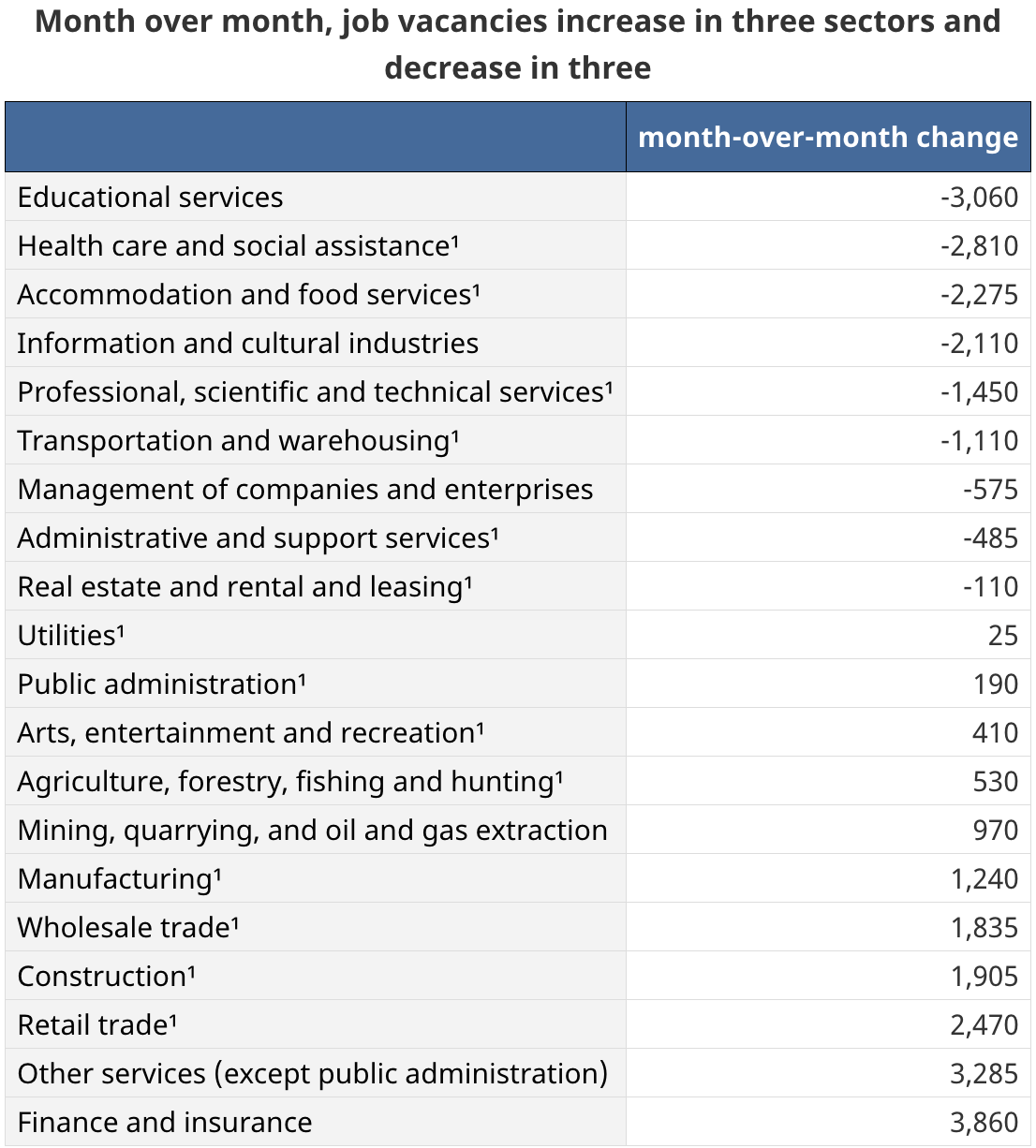

Job vacancies were largely unchanged in February. Statistics Canada reported 497,200 vacant positions, “little changed from January.” On a year‑over‑year basis, job vacancies were down 29,000 (-5.5%), a decline the agency described as “significantly lower than the decline from February 2024 to February 2025 (-124,600; -19.1%).”

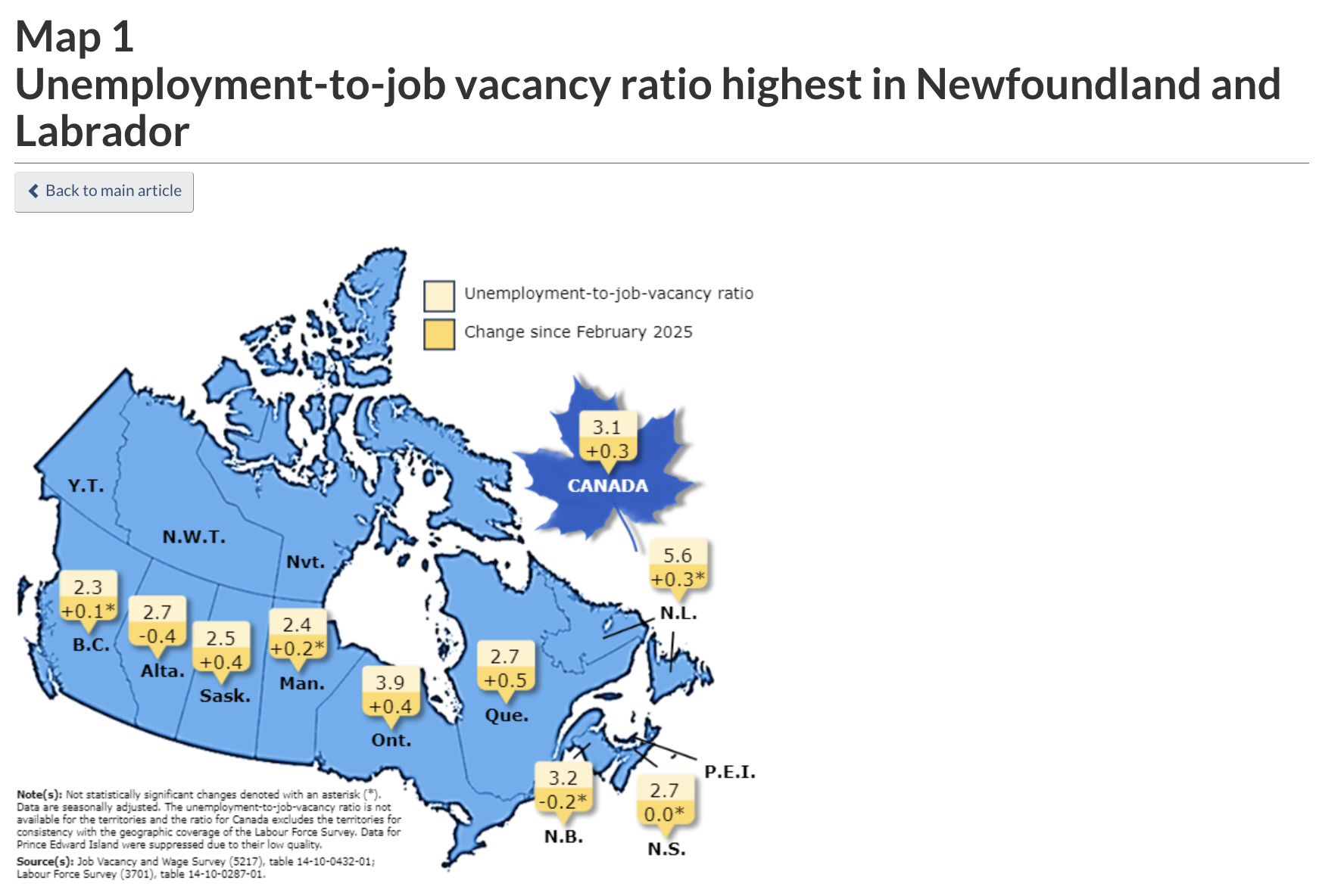

The national job vacancy rate was 2.8% in February 2026, unchanged from January and down 0.1 percentage points from February 2025 (2.9%). There were 3.1 unemployed persons for every job vacancy in February, up 0.1 from January and 0.3 higher than a year earlier, with the ratio remaining in a narrow range of 3.0 to 3.1 from November 2025 to February 2026.