‘Workplace plans matter to participants, and many still do not feel confident making the right decision on their own’

HR professionals administering workplace retirement plans may want to make some adjustments, as many workers are looking for simpler and better solutions, based on the findings of a recent survey.

Overall, 73% of defined contribution plan participants wish they could fully delegate their retirement planning and investing decisions, according to J.P. Morgan Asset Management's 2026 Defined Contribution Plan Participant Survey.

"This ongoing research is important for retirement planning conversations because it captures direct feedback from participants at every stage of the retirement journey," said Alyson Frost, Head of Retirement Insights at J.P. Morgan Asset Management. "Workplace plans matter to participants, and many still do not feel confident making the right decision on their own. They want retirement decision-making made simpler, and they welcome support from their plans in turning savings into retirement income."

Generational divide in expectations

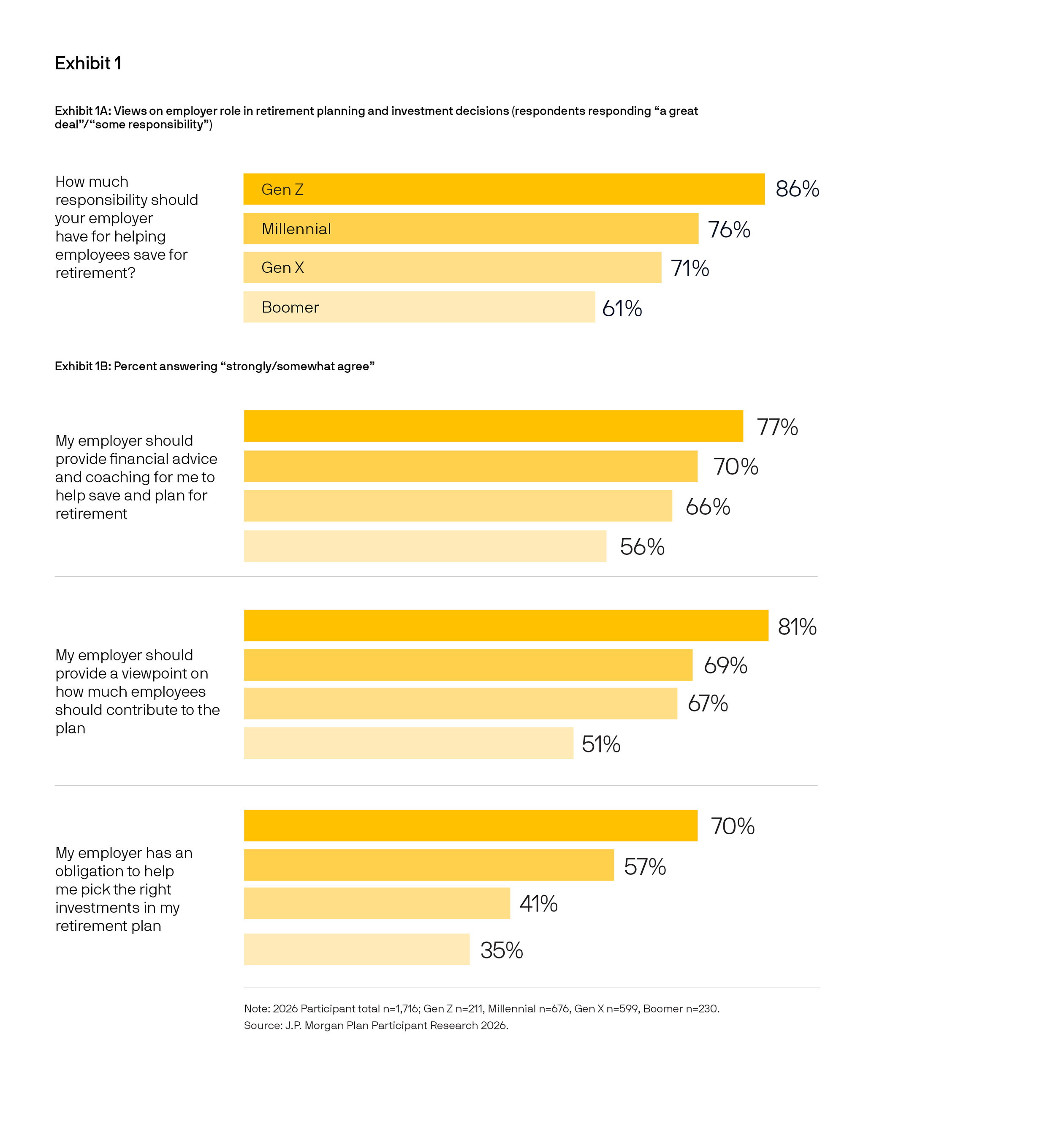

There is also a widening gap in how much responsibility workers across generations believe employers should bear for retirement readiness, according to J.P. Morgan Asset Management’s survey of over 1,700 U.S. respondents.

Among Gen Z respondents, 86% said their employer has a great deal or some responsibility to help them save, compared with 61% of Boomer respondents, according to J.P. Morgan Asset Management. The share of participants wanting to "push an easy button" and delegate retirement decisions entirely rose to 73% this year, up from 55% in 2016, suggesting younger employees will expect more built-in guidance than earlier cohorts required.

J.P. Morgan Asset Management reported that "the largest share of participants (44%) expects to retire gradually by reducing how much they work over time, but only 12% of retirees report this as their actual transition experience," a gap relevant to employers designing phased retirement policies.

Fewer than half of workers have an employer-sponsored pension and most lack even a basic retirement plan, according to a previous report.

Guaranteed income solutions, savings gap

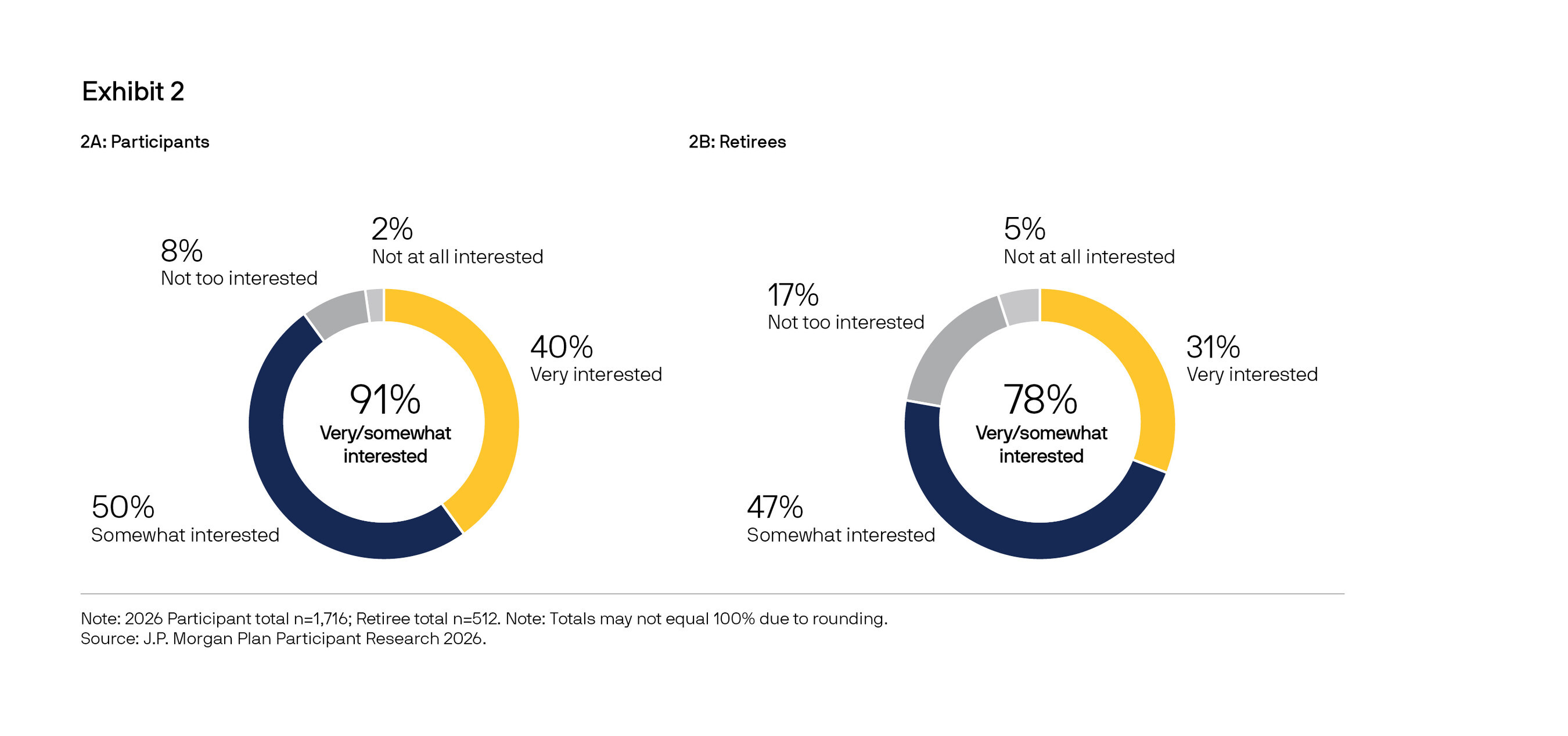

A total of 91% of participants expressed interest in in-plan guaranteed retirement income solutions, and 75% said they would likely keep assets in the plan if such an option were offered, reported J.P. Morgan Asset Management.

The survey also found declining confidence in Social Security, with only 35% believing their benefits will cover routine expenses. The finding has relevance for Canadian employers communicating about government retirement benefits.

The survey pointed to a persistent savings gap. It found 59% believe they should contribute more, 63% of retirees wish they had contributed more while working, and 53% do not know how much they need to save to retire securely. Automatic plan design features showed strong satisfaction results: 96% of participants who were automatically defaulted into their plans and 97% of those with automatic contribution escalation reported being satisfied, evidence supporting expanded auto-enrolment provisions.

The survey also linked financial stress to plan leakage: 45% of participants who took a plan loan did so to cover unexpected expenses or credit card debt, and those without emergency savings were almost 70% more likely to have taken a loan or withdrawal.

Canadian workers are routinely undervaluing their workplace retirement plans because of how employers and plan sponsors communicate them — and that this is happening despite retirees saying they “couldn’t live without” that income, according to a previous report.

Retirement readiness matters to every Canadian, “not only to ensure a secure financial future but also to sustain a resilient economy and standard of living that remains the envy of the world,” the CAAT Pension Plan said in a report previously emailed to HRD.

Retirement readiness matters to every Canadian, “not only to ensure a secure financial future but also to sustain a resilient economy and standard of living that remains the envy of the world,” the CAAT Pension Plan said in a report previously emailed to HRD.

“When people feel confident about their future in retirement, they are more able to participate fully in the economy today and tomorrow. This connection between financial security and economic resilience is becoming harder to ignore in Canada, already one out of five people is 65 years or older designating us as a super-aged society, and where one out of four people will be 65 years or older by as early as 2043.”