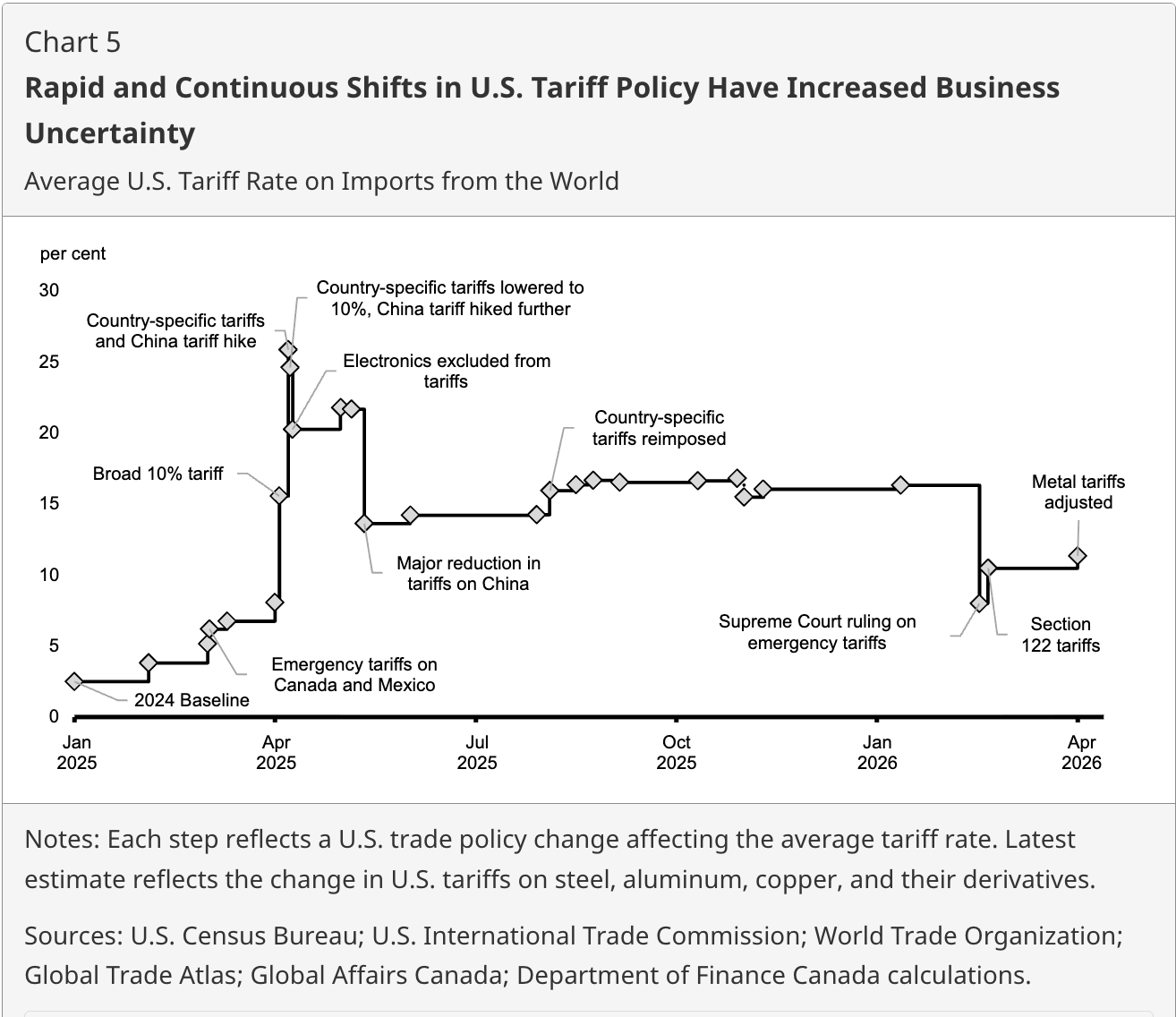

Global economy ‘is more than a year into a profound rupture’

Canada’s economy avoided recession in 2025 and continues to generate jobs at a faster per‑capita pace than the United States, according to the federal government’s Spring Economic Update 2026.

Real GDP grew by 1.7% in 2025 despite higher U.S. tariffs, trade tensions and global instability linked to the conflict in the Middle East. “The economy avoided a recession and domestic activity remained solid, even as tariff increases and trade tensions weighed on activity,” the federal government said.

Labour market conditions “have remained resilient,” the update states. Since the start of 2025, “Canada has added nearly three times as many jobs per capita (3.4 per 1,000 of population) as the U.S. (1.2 per 1,000).” The majority of those jobs have been in the private sector.

The national unemployment rate, which peaked at 7.1% in September 2025, declined to 6.7% as of March 2026, better than private sector expectations at the time of Budget 2025. The government says “businesses and workers have shown remarkable resilience in the face of significant uncertainty.”

Canadian manufacturers in heavily tariffed industries are seeing declining or stagnant employment despite mixed trends in output and rising prices, with auto, metals and forestry workforces under the greatest strain from the U.S. tariffs, according to an RBC Economics report.

Wages, participation and pressure points

The report from Ottawa highlights sustained gains in employee purchasing power. “Wage growth has now outpaced inflation for more than three consecutive years, supporting continued gains in real incomes,” the update notes. Real wages have risen by an average of 1.6% per year since 2023, nearly double the pre‑pandemic pace.

Canada continues to lead major peers on participation. The labour force participation rate stands at 64.9%, above the U.S. rate of 61.9%, with women’s participation in the 25‑to‑54 age group reaching 85% in 2025 — nearly seven percentage points higher than in the United States.

At the same time, the update points to ongoing strains. Youth unemployment stands at 13.8% as of March, down only slightly from a peak of 14.6% in September 2025. Demand is “particularly soft for entry-level jobs, a headwind for both youth and newcomers,” the report states.

Tariff‑exposed industries such as steel, softwood lumber and motor vehicles and parts have seen job losses, while residential construction employment declined by 6.2% in Ontario and 2.6% in British Columbia in 2025. The government says maintaining construction capacity is “essential to scaling up housing supply and securing durable affordability gains nationwide.”

Despite these challenges, initial Employment Insurance claims remain within historical norms, and “many displaced workers are finding new employment,” according to the federal government. The 2026–2028 Immigration Levels Plan is expected to keep population growth at more sustainable levels, supporting what the update describes as a more balanced labour market.

Outlook and fiscal position

The government says the global economy “is more than a year into a profound rupture,” with economic security concerns and geopolitical competition reshaping investment and trade. The conflict in the Middle East has disrupted shipping through the Strait of Hormuz and pushed energy prices higher.

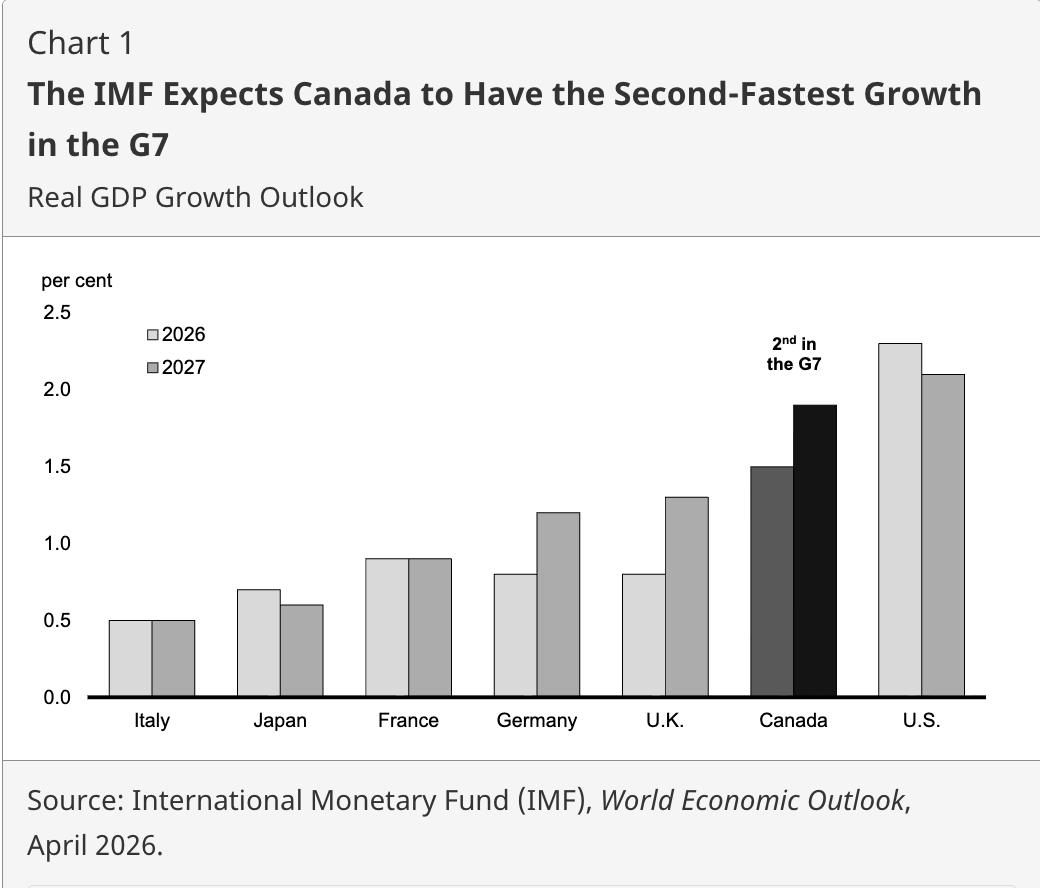

Even so, private sector forecasters expect Canadian real GDP to grow by 1.1% in 2026 and 1.9% in 2027. The International Monetary Fund projects Canada will post the second‑fastest growth in the G7 over 2026 and 2027.

Inflation averaged 2.1% in 2025 and has stayed within the Bank of Canada’s 1–3% target band for 27 consecutive months. On the fiscal side, stronger‑than‑expected nominal GDP and higher oil prices have improved the outlook, narrowing the projected 2025–26 deficit to $66.9 billion, or 2.1% of GDP, an $11.5‑billion improvement from Budget 2025.

Earlier this year, Ottawa announced it is investing up to $94.5 million over five years to improve labour market intelligence across major economic sectors, in a move aimed at helping employers and workers better respond to skills shortages and shifting market conditions.