'They're engaged and taking their financial future seriously while navigating through turbulence'

Despite Canadians’ current financial struggles, most are still looking to ensure financial wellness far into the future, according to a report.

Canadians are making adjustments to their investment strategies rather than withdrawing from their retirement plans, reports Sun Life, based on an analysis of 1.5 million group retirement plan members.

“In Q1 2025, members moved their money out of U.S. equity funds at the highest rate witnessed since the beginning of the COVID-19 pandemic,” notes the financial services company. “While more people are reducing their risk exposure, they are not withdrawing their money from their plans. Withdrawal rates remain stable when compared to past years.”

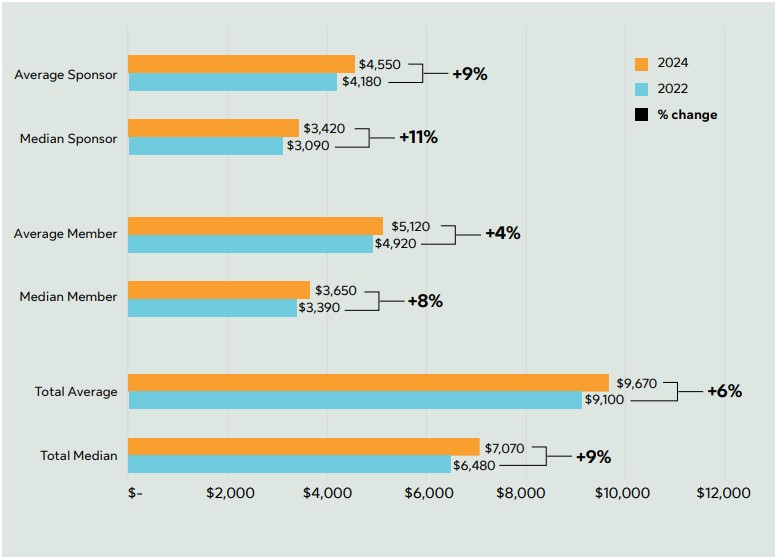

Despite economic headwinds, combined contributions climbed 6% to an average of $9,670 since 2022, with members contributing $5,120 and sponsors adding $4,550 on average, according to the report.

Target date funds (TDFs) remain a popular choice, now holding 42% of plan member balances, up from 29% in 2018. Members investing solely in TDFs have outperformed those in non-target date funds in eight of the past ten years.

“The ‘buy Canadian’ sentiment that gained popularity earlier this year may also be having an impact on how people are investing their money. While some are adjusting their finances, it’s encouraging to see that they aren’t reactively pulling their money out of the market,” says Dave Jones, senior vice-president, Group Retirement Services, Sun Life. “Some Clients are shifting their assets from U.S. equities into more conservative options. They’re engaged and taking their financial future seriously while navigating through turbulence.”

The number of Canadians enrolled in registered pension plans (RPPs) has surpassed the 7.2 million mark, according to a previous Statistics Canada (StatCan) report. And amid Canadians’ worries about saving for their post-work life, contributions to registered retirement savings plans (RRSPs) are on track to hit a record high this year, according to a separate report from BMO Financial Group.

Workplace savings plans

The report also found that members of workplace savings plans are retiring, on average, two years earlier than the average Canadian.

Sun Life recommends that employees take full advantage of workplace savings plans, create personalised financial plans, and connect with advisors to help secure their financial future.

The average workplace plan account balance has grown to $94,220, a 16% increase since 2022, according to the report.

“In times of change and uncertainty, having a trusted partner who understands your unique goals and needs is paramount,” says Rowena Chan, president, Sun Life Financial Distributors (Canada) Inc. and senior vice-president, Retail Advice & Solutions.

Despite the positives, 80% of Canadians say the rising cost of living makes it difficult to save for retirement, according to a previous IG Wealth Management study.

Here are some ways employers can support workers in the area of saving for retirement, according to WEX Benefits, a provider of a commerce platform:

- Offer a benefits package with employer contributions.

- Provide financial wellness education.

- Implement auto-enrolment and auto-escalation in workplace savings plans.

- Encourage smart benefit utilisation.

“Employers play a crucial role in helping employees balance their healthcare and retirement savings goals. By offering the right mix of benefits, education, and incentives, you can empower your workforce to build financial security for both the short and long term,” says WEX Benefits.

“When employees feel confident about their financial future, they are more engaged, productive, and loyal—creating a win-win for everyone.”