Flexible savings options, annuity‑like solutions like VPLAs and broader diversification 'can create a truly powerful DC retirement ecosystem’

New design features in defined contribution (DC) retirement plans could allow some Canadians to retire three or more years earlier than under traditional arrangements, according to Mercer’s 2026 Retirement Readiness Barometer.

The analysis finds that combining flexible plan design, broader exposure to alternative investments and new decumulation options such as Variable Payment Life Annuities (VPLAs) can significantly improve retirement readiness across income levels.

Mercer positions these developments as a way for workplace plans to better support retirement security without compromising member control or flexibility.

“This year’s Barometer illustrates that innovation in DC is aligning to better support retirement and savings outcomes,” says Bernadette Chik, Mercer Canada’s Defined Contribution Leader. “By offering flexible savings options, access to annuity‑like solutions like Variable Payment Life Annuities (VPLAs) and broader diversification through alternative assets, employers can create a truly powerful DC retirement ecosystem.”

Employers should become more proactive when it comes to preparing workers for retirement, as fewer than half of working-age Canadians have an employer-sponsored pension and most lack even a basic retirement plan, according to a previous report.

‘Retirement and savings outcomes’

The 2026 Mercer Retirement Readiness Barometer uses proprietary Mercer retirement readiness analytics to measure the age at which different worker personas can comfortably retire, based on participation in employer‑sponsored capital accumulation plans and government benefits such as CPP, QPP and OAS.

Retirement readiness in the Barometer is defined as a 75 per cent probability of not running out of money before death if an appropriate level of income is maintained throughout retirement, including public benefits.

Mercer says this year’s Barometer “illustrates that innovation in DC is aligning to better support retirement and savings outcomes,” particularly when flexible design, diversified investments and decumulation options are combined.

Canada's Defined Contribution (DC) Pension System — At a Glance

|

Category |

Detail |

|

Employer and employee contributions (if any) are defined; pension income at retirement is determined largely by the contributions and investment income accumulated. Contributions are often a fixed percentage of annual earnings, deposited monthly in an individual account in the member's name. |

|

|

Who bears the risk |

Member bears investment and longevity risk; employer's obligation ends at the contribution. |

|

Federal regulator |

Office of the Superintendent of Financial Institutions (OSFI) — for federally regulated industries (banking, interprovincial transport, telecoms, federal Crowns). Provincial regulators cover the rest. |

|

Tax registration |

All DC plans are registered with the Canada Revenue Agency (CRA); contributions are tax-deductible and growth is tax-deferred. |

|

2024 contribution cap (Money Purchase limit) |

The 2024 money purchase (MP) limit is $32,490; effective cap is the lesser of 18% of earnings or the MP dollar limit. |

|

Pension Adjustment (PA) |

DC contributions in a year reduce the member's RRSP room the following year. |

|

A locked-in RRSP or locked-in RRIF, an annuity, or (where allowed) a variable benefit paid from the plan; small balances may be unlockable. |

|

|

Locking-in |

Funds typically locked until ~age 55, subject to provincial/federal pension legislation. |

|

Pooled Registered Pension Plans are provided by licensed administrators to employees of multiple employers and to self-employed persons. Contributions are often a fixed percentage of the member's annual earnings and are deposited monthly in an individual account in the member's name. |

A previous report warned that Canadian workers are routinely undervaluing their workplace retirement plans because of how employers and plan sponsors communicate them — and that this is happening despite retirees saying they “couldn’t live without” that income.

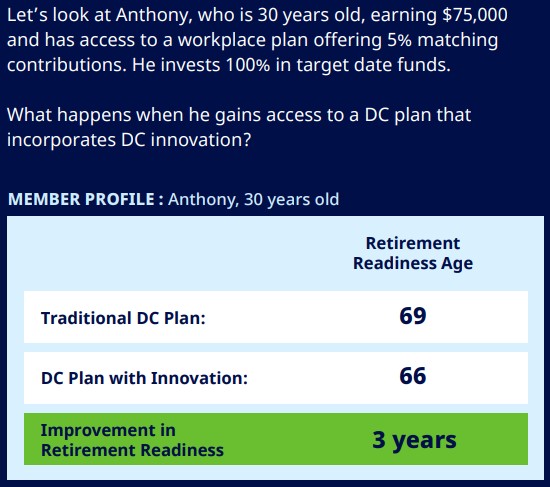

Two DC scenarios for a typical Canadian worker

Mercer compares two workplace plan designs using a sample persona, “Anthony,” a 30‑year‑old Canadian earning $75,000, investing 100 per cent in target date funds and eligible for a 5 per cent employer matching contribution.

In the traditional workplace plan, Anthony delays participation and contributions for 15 years, then saves 10 per cent of pay (5 per cent employee and 5 per cent employer). His target date fund has 5 per cent exposure to alternative investments, and at retirement he converts his savings to a traditional drawdown vehicle.

In the innovative workplace plan, Anthony saves 5 per cent from the start of his career (5 per cent employee and 5 per cent employer), with the ability to access savings for short‑term needs during the first 15 years, then 10 per cent thereafter as his finances improve. The target date fund has 15 per cent exposure to alternatives, and at retirement he has access to a VPLA product to convert his savings into income.

Flexibility, alternatives and VPLAs drive gains

Mercer says this “smarter DC ecosystem” improves Anthony’s retirement readiness age from 69 under the traditional plan to 66 under the innovative design, a three‑year gain. For higher earners, Mercer reports that “the impact is even greater, resulting in improved retirement readiness by as much as 5 or more years.”

The firm identifies three main innovations: flexible DC plan designs that “enable members to save for multiple goals, boosting participation and increasing plan value across diverse demographics”; enhanced investment outcomes through “broadened exposure to alternatives in target date funds”; and options at retirement to convert a portion of savings into Variable Payment Lifetime Annuities, “creating stable income and greater security in retirement.”

Mercer notes that “as target date funds broaden their allocations into alternatives including private markets, everyday investors can increasingly access and benefit from a growth source that was previously available only to institutional and large investors.”

Regulatory changes and employer next steps

The Barometer points to “recent updates to regulations – paving the way for the possibility of converting a portion of savings into VPLAs,” with DC plan members able to benefit from longevity pooling “to reduce the risk of outliving their savings.”

Mercer adds that “with both of these innovations, DC plan members maintain control and can tailor both their accumulation and decumulation experience for their financial journey,” underscoring that members are not locked into a single approach.

The firm urges employers to “explore ways to improve plan member outcomes in your DC plan,” focusing on plan design flexibility, the role of alternatives in target date funds and access to VPLA‑type decumulation options. Mercer concludes that “together, these innovations position DC plans as the flexible retirement and savings benefit that can support the financial wellness of a diverse workforce and allow Canadians to shape retirement income and spending on their own terms.”

Coverage and Membership Data (Federal Sources, 2023)

|

Indicator |

Value |

|

Active RPP members in 1993 → 2013 → 2023 |

5.2 million → 6.2 million → 7.2 million |

|

Women's share of RPP members (2023) |

|

|

RPP coverage as % of labour force (2023) |

34% |

|

RPP coverage as % of employees (2023) |

|

|

Coverage including Group RRSPs / DPSPs (employees) |

51% |

|

DC plans' share of total RPP membership (2023) |

18.6% (up 0.2 pts from 2022) |

|

DC membership growth (2023) |

+65,300 members (+5.1%) |

|

Private-sector share of DC membership |

~86.7% |

|

Members in hybrid / other plan types, 2004 vs. 2023 |

179,000 → 963,000 (85% private sector in 2023) |

Aggregate RPP Financials (2023)