Lower contribution rate would free up funds for private savings, says Frasier Institute

Alberta workers could significantly boost their retirement income by moving from the Canada Pension Plan (CPP) to a provincial pension plan, according to a new report from The Fraser Institute.

“Due to Alberta’s comparatively high rates of employment, higher average incomes, and younger population, Albertans would pay a lower contribution rate through a separate provincial pension plan while receiving the same benefits as under the CPP,” said Tegan Hill, director of Alberta policy at the Fraser Institute and co-author of the report titled Illustrating the Potential of an Alberta Pension Plan.

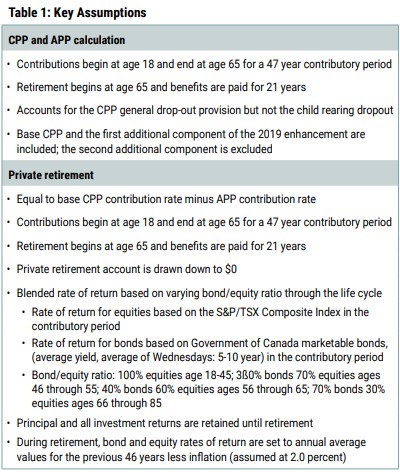

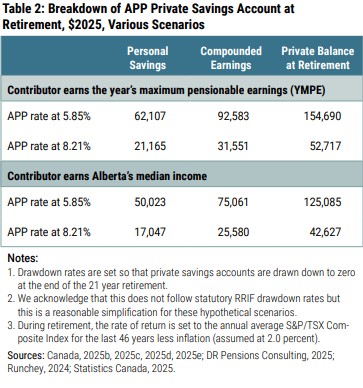

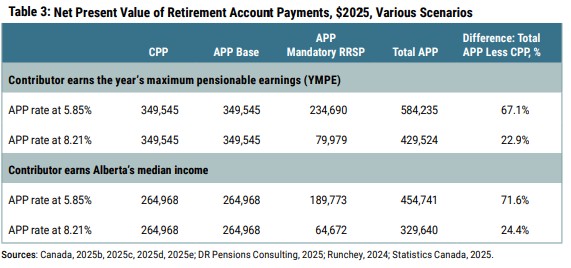

In comparing the potential retirement income of Albertans under the CPP to what they could receive if the province established its own pension plan (APP) with identical benefits but lower contribution rates, the analysis uses two contribution rate scenarios—5.85% and 8.2%—based on recent estimates.

The report found that a median-income Albertan retiring in 2025 could see their total pre-tax retirement income rise by 71.6%—up to $454,741—if the APP contribution rate is set at 5.85% and the savings are invested privately. This compares to $264,968 under the CPP alone.

Even with a higher APP contribution rate of 8.2%, the same worker would see a 24.4% increase in retirement income, totalling $329,640.

The Fraser Institute notes that the APP would offer the same defined benefit as the CPP, but the lower contribution rate would free up funds for private savings, giving Albertans more control over their retirement planning. The report also highlights that private savings allow for more flexible withdrawals and the potential for continued investment growth during retirement.

Despite Canadians’ current financial struggles, most are still looking to ensure financial wellness far into the future, according to a report. Canadians are making adjustments to their investment strategies rather than withdrawing from their retirement plans, reports Sun Life, based on an analysis of 1.5 million group retirement plan members.

Four in 5 (80%) of Canadians say the rising cost of living makes it difficult to save for retirement, according to a previous IG Wealth Management study.

Retirement Planning and Resources

Earlier this year, the federal government launched the Retirement Planning and Resources advertising campaign, which promoted the availability of a range of retirement planning tools and resources to Canadians.

“Whether planning for retirement or already enjoying it, Canada.ca/retirement will help Canadians explore public pension programs, retirement checklists, budget planning, retirement calculators and more to help make the most of their retirement, no matter where they are in their journey,” according to the federal government.

Topics covered in the campaign—which ran Feb. 17 to March 23—included:

- public pensions, such as the Canada Pension Plan (CPP), Old Age Security (OAS) and the Guaranteed Income Supplement (GIS), and how to apply;

- the Retirement Income Calculator and OAS Benefits Estimator;

- employer pension plans and how much workers may need to save;

- tools from the Financial Consumer Agency of Canada, such as the Retirement Checklist and the Budget Planner;

- transitioning from working to retirement;

- retiring abroad and receiving public pensions outside of Canada;

- managing public pensions when already retired;

- payment dates for CPP and OAS;

- eligible tax deductions and benefits;

- frauds and scams; and

- protecting yourself from financial abuse.