HRD analysis of ABS data reveals a labour market fracturing along state lines. A single national strategy is no longer enough

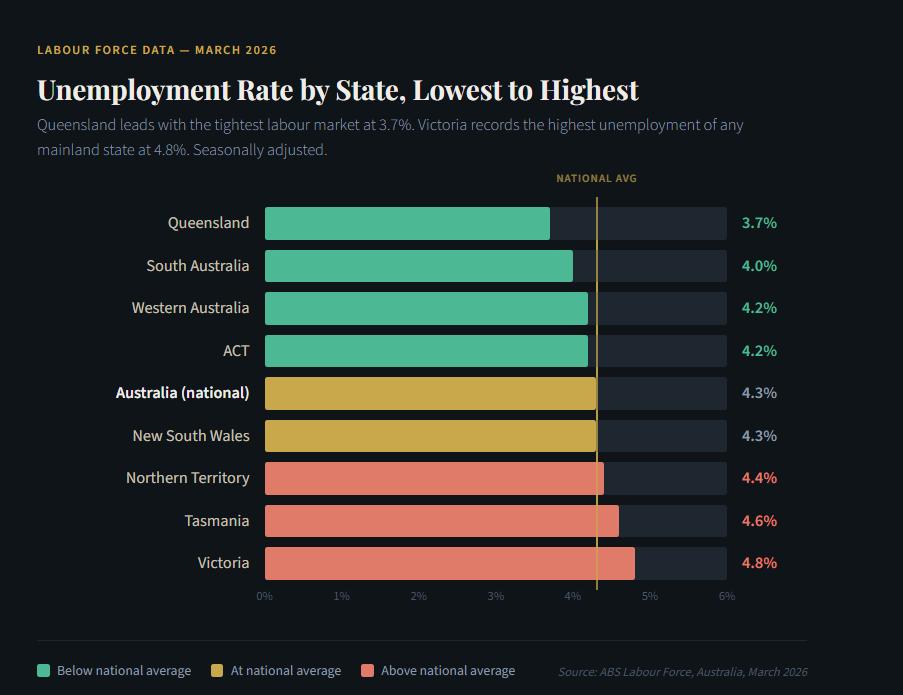

There is a temptation, when scanning national employment figures, to treat Australia's labour market as a single entity. Our analysis of the latest data from the Australian Bureau of Statistics says – not so fast…. Beneath a stable headline unemployment rate of 4.3% lies a set of state and territory figures that tell quite different stories — about demand, tightness, and the conditions in which HR professionals in different parts of the country are actually operating.

If your company has a national footprint, or if you are considering geographic expansion of your workforce, the latest ABS figures are not background reading. They are a planning document.

Queensland: The standout performer

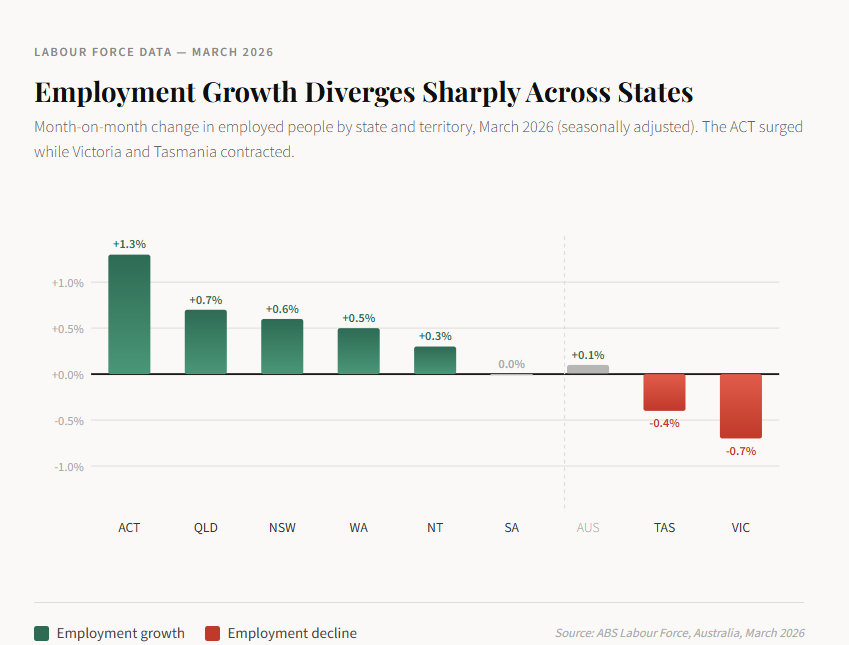

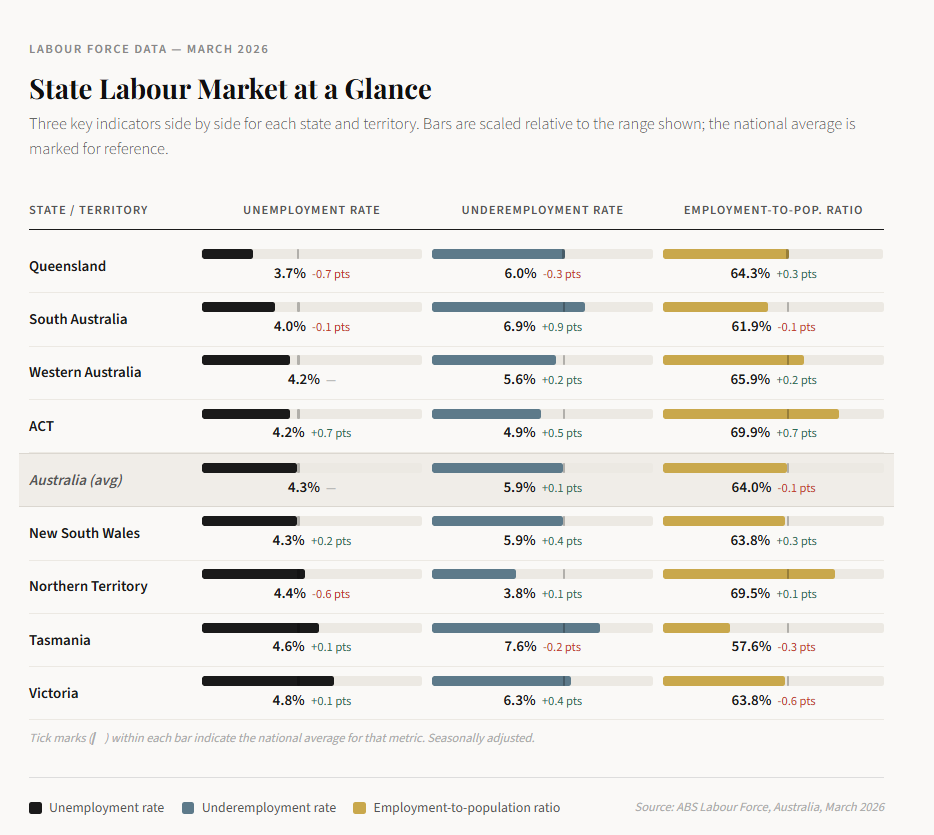

The most striking single-state result from the March release belongs to Queensland. The state's unemployment rate fell 0.7 percentage points in the month to reach 3.7% — the lowest unemployment rate of any state or territory in mainland Australia and a figure that represents a genuinely tight labour market by any historical measure.

Trend employment in Queensland rose 0.3% in March, adding approximately 9,100 persons to the workforce. This continues a pattern of solid, sustained employment growth that has been a feature of the Queensland labour market throughout the post-pandemic period. The state continues to benefit from interstate migration, which expands its labour force and supports steady hiring demand across construction, community services, health, logistics, and regional roles — sectors that collectively account for a large share of Queensland employment.

Read next: Are you ready for a deluge of new employment regulation?

For HR leaders with Queensland operations, the data has two implications. Workforce planning should assume a competitive external hiring environment will persist; applicant pools for skilled roles are unlikely to deepen materially in the near term. Retention investment therefore carries a higher return than it might in a looser market. Equally, with underemployment at 6.0% — itself above the Western Australian figure — there remains a meaningful pool of employed Queenslanders seeking additional hours, particularly in regional centres where the labour market dynamics differ from those of greater Brisbane.

Victoria: The signal worth watching

Victoria's March figures warrant particular attention, and not only because they diverged sharply from the national trend. Employment in the state fell 0.7% over the month — the largest state-level decline recorded in the March release. The participation rate dropped 0.6 percentage points, and the unemployment rate ticked upward by 0.1 points to 4.8%, the highest of any state bar Tasmania.

These are monthly figures, and monthly volatility is a feature, not an anomaly, of labour force data. They should not be overinterpreted in isolation. Nevertheless, the direction of travel in Victoria merits attention from employers and HR professionals operating in Melbourne and its broader economy.

Talent International's 2026 workforce outlook identified a somewhat cautious picture for Victoria entering the year, noting that while underlying demand in healthcare, construction, education, and technology remains strong, the benefits of that demand are not evenly distributed. Success, the report suggested, would increasingly hinge on targeted skills alignment and flexibility. That assessment finds some corroboration in the March employment figures.

There is, however, a structural development in Victoria that HR professionals cannot afford to ignore regardless of short-term employment data. The Victorian government has confirmed that legislation enshrining a legal right to work from home two days per week will take effect from 1 September 2026, with a delayed commencement of 1 July 2027 for workplaces with fewer than 15 employees. The right will be embedded in the Equal Opportunity Act, shifting flexible work from an employer discretion to a legal entitlement for employees who can perform their role remotely.

For Melbourne-based employers, the practical implication is that HR policy, employment contracts, and role definitions will require review well before September. Organisations that have clear frameworks for hybrid work are better positioned to manage this transition; those relying on informal arrangements face the risks of inconsistency, non-compliance, and employee grievances that the Aon human capital team has warned are particularly acute for smaller businesses.

Employee exits in Victoria are disproportionately attributed to limited career opportunities (38 per cent of Victorian employers cited this as the primary driver of turnover, the highest of any state). That finding, combined with the incoming right-to-work-from-home legislation, frames a specific challenge for Victorian HR functions: retaining experienced employees requires both genuine development pathways and demonstrably flexible working arrangements. The data suggests neither can be treated as optional.

Western Australia: Tight and getting tighter

Western Australia continues to present the most compressed labour market conditions of any mainland state. An employment-to-population ratio of 65.9% — the highest in Australia — alongside an unemployment rate of 4.2% and an underemployment rate of just 5.6% leaves limited slack in the system for employers seeking additional capacity.

Western Australia recorded the fastest pace of wage growth of any state through to end-2025, at 3.6% annually — a reflection of the competitive pressure that persistent labour market tightness places on remuneration. For employers in the resources, construction, and professional services sectors that dominate Perth and the regions, salary benchmarking should be treated as a live activity rather than an annual exercise. The cost of losing skilled employees to competitors in a market this tight is not simply a recruitment cost; it is an operational risk.

Jobs and Skills Australia's employment projections to 2035 flag Western Australia for particularly strong growth in mining employment, reinforcing the view that pressure on specialist technical labour will be a persistent feature of the Western Australian market for the foreseeable future.

New South Wales: Cautious optimism, rising competition

New South Wales returned broadly neutral figures in March. Employment grew 0.6% — one of the stronger monthly results — but an underemployment rate of 5.9% and an unemployment rate of 4.3% place the state squarely at the national average. The labour market is neither deteriorating nor tightening.

Job vacancies in New South Wales rose 3.8% in the three months to February 2026, consistent with solid underlying demand. However, talent industry analysis has noted that NSW has seen one of the more pronounced falls in job advertising volumes compared with other metropolitan markets over the past year, and that hiring processes have become more measured — with employers taking longer to decide and candidates facing more competition for roles offering stability.

The turnover picture in NSW is notably fragmented: career development, lack of training, uncompetitive salary, and work-life balance all feature as leading drivers of attrition, without any single factor dominating as it does in some other states. This suggests that retention programmes in New South Wales benefit from a multi-dimensional approach rather than single-lever interventions such as salary adjustment alone.

The ACT: Public sector uncertainty reshapes the market

The Australian Capital Territory posted the most unusual result of any jurisdiction in the March data. Participation surged 1.3 percentage points — the largest monthly increase recorded — while unemployment simultaneously rose 0.7 points to 4.2%. The most plausible reading of this combination is that a wave of people re-entered the labour force but had not yet secured employment at the time of the survey.

This reading is consistent with broader analysis of the ACT labour market, which has been shaped by a significant contraction in government and defence job advertising over the past year. The ACT has been identified as the jurisdiction feeling the largest impact from reduced public sector hiring, with vacancy levels in government roles now below pre-COVID levels. For private sector employers in Canberra, this dynamic has a silver lining: larger applicant pools and improved access to talent — including highly experienced public sector professionals seeking transition — are likely to characterise the hiring environment through 2026.

The national hiring backdrop

Against this varied state-level picture, the national hiring environment remains broadly active. More than 82% of Australian employers plan to recruit in 2026, with replacement hiring — rather than growth — now the dominant driver. Total job vacancies nationally reached 337,900 in February 2026, the highest level in more than a year, led by construction, retail trade, and accommodation and food services.

That activity is occurring, however, against a labour market that the Commonwealth Bank's Economics team has characterised as "slightly tight" — a description that conceals significant regional variation. For HR functions managing multi-state operations, the implication is that a single workforce strategy calibrated to national averages will systematically misallocate effort: too conservative in Western Australia and Queensland, potentially too aggressive in Victoria and the ACT, and roughly appropriate only in the states that happen to sit near the median.

Practical implications for HR leaders

State-level labour market divergence has several concrete implications for workforce planning.

Compensation benchmarking must be geographically granular. A salary band calibrated to a national median is likely to be uncompetitive in Perth and overgenerous in Canberra. Where enterprise agreements permit, location-based adjustments for particularly tight markets warrant consideration.

Retention investment should track tightness. The probability that a departing employee can be replaced quickly and cost-effectively is materially lower in Queensland and Western Australia than in the ACT or Victoria at present. Organisations should weight their retention programme intensity accordingly, rather than applying uniform investment across all locations.

Victoria's legislative changes require immediate HR attention. The incoming right-to-work-from-home legislation is not a 2027 problem. Policy development, contract review, and manager training require lead time, and September 2026 is closer than it appears on a planning horizon.

The ACT and Victoria represent talent sourcing opportunities. In a national market where 75% of Australian businesses report greater difficulty finding qualified local talent than a year ago, the availability of experienced workers in softer markets should factor into sourcing strategies — particularly for remote or hybrid roles that are not geographically constrained.

The March 2026 figures confirm what experienced workforce planners have long understood: Australia is not one labour market. It is eight, each with its own dynamics, pressures, and opportunities. The organisations best positioned to navigate what remains a demanding environment are those that plan at that level of granularity.